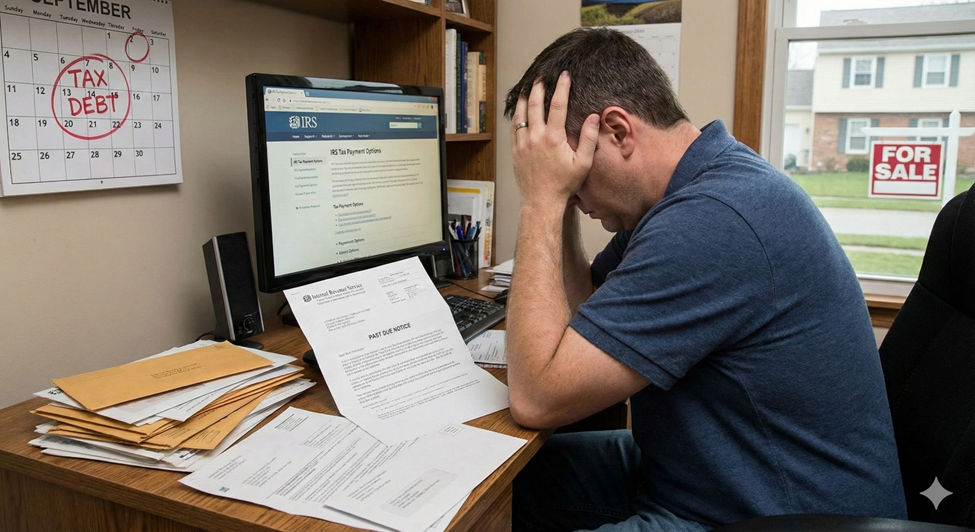

Do the Old Tax Debts Finally Expire in the US?

The burden of a pending tax debt can be interminable. But what would happen when there was an expiry date? The positive side of it is that the IRS and the California Franchise Tax Board (FTB) have a legal time constraint, the so-called statute of limitations, within which it has to collect a tax debt.

Knowledge of such timelines and the manner in which they are manipulated is paramount in the case of any taxpayer going through financial difficulties. In this blog, we are going to subdivide the key deadlines of federal and state tax debt and discuss the actions that are likely to extend the collection clock dramatically. Always look for a tax expert (like an EDD audit attorney) whenever you are in trouble.

Understand the Collection Statute Expiration Date

The major regulation in the case of the IRS is the 10-year Collection Statute Expiration Date (CSED). This is not a random countdown, but it commences on the official assessment date of the tax, which is normally on the date your tax return was actually submitted or when a tax bill was prepared following an audit.

Key Aspects You Need to Know About IRS CSED

The period of 10 years is normally fixed upon the original assessment date.

- After expiration, the collection of the debt by the IRS is not possible anymore under the provisions of the law by levying, garnishing wages, and other imposed measures of collection.

- The uncollectable debt must be marked and cease collection by the IRS after the CSED is passed.

- Nevertheless, the journey towards this finish line is not a straight road to success. Some acts may tend to pause or lengthen this 10-year clock, which gives the IRS more time to collect.

See also: Navigating Hot Water Repairs: Essential Tips for Homeowners

Check the Californian Clock

- The Californian taxpayers have a different and sometimes prolonged collection interval. The first collection statute of the FTB is also an assessment date of 10 years. There is, however, a critical distinction in the strength of liens.

- After the FTB registers a state tax lien, it will have 10 years to collect the lien, starting on the date when the lien is recorded.

- In addition, in case the lien is renewed prior to its elapsing, another 10 years may be added to the collection period. This forms a possible scenario of tax liability for those 20 years and above.

- This renders proactive California tax debt settlement even more of a necessity since the capacity of the state to collect tax has a significantly longer prospective than the IRS.

Can We Reset the Collection Clock?

The indication of an expiration date may be deceptive unless you know what things may be done to extend the timeframe. The IRS and FTB have the legal right to extend the period of collection based on particular activities of the taxpayers. Consult with an experienced tax professional who can help you with a CDTFA audit.

Actions We Can Take

Ordinary acts that make the statute of limitations toll or run include:

- The time is stopped at the time of consideration of the OIC, and 30 days after the OIC is rejected. The rejection does not stop the tolling, but on appeal.

- An automatic stay is created, which postpones any collection and tolls the statute of limitations until the entire process of the bankruptcy is done, as well as for six months.

- An appeal of a notice of a levy on the basis of a CDP hearing will not result in the collection clock being stopped, as your case is considered.

Seek the advice of a professional tax practitioner, CPA, or tax attorney. They can assist you in negotiating your particular scenario, validate the appropriate CSED, and formulate a plan that will either take advantage of the expiring clock or cope with the results of action that may lengthen it. Then do not allow a technicality to be a trap–seek expert counsel to know your real way to financial freedom.